{kind=link}

BRAZIL – 2019/12/05: In this photo illustration the CenterPoint Energy logo is seen displayed on a … [+]

CenterPoint Energy (NYSE: CNP), a utility holding company that operates in markets including Texas and Indiana, has seen its stock price recover by about 70% from its March 2020 lows and currently trades at about $21 per share. However, the stock remains down by about 20% over the last twelve months, partly due to weaker commercial and industrial electricity demand through the Covid-19 lockdowns and the company’s move to cut its dividend. However, we think the stock looks reasonably priced at current levels, considering its relatively lower valuation versus peers, its plans to divest its underperforming business, and a broader economic recovery post-Covid-19.

CenterPoint Energy’s stock price has declined by about 25% since 2017. There are multiple factors driving the decline. The company’s revenues grew from around $9.6 billion in 2017 to about $12.3 billion in 2019, driven partly by its acquisition of Vectren, an Indiana-based utility company. However, revenues have declined over the last twelve months, to $12.1 billion, due to lower demand for electricity among commercial and industrial users. While the company’s reported net income has been volatile due to the effect of tax and one-time items, its adjusted EPS has grown steadily from around $1.37 in 2017 to $1.79 in 2019, although it declined to about $1.50 over the last twelve months. Now CenterPoint’s P/E multiple has declined from around 21x in 2017 to 15x in 2019 to about 14x currently (based on trailing twelve months adjusted earnings. Our dashboard, ’What Factors Drove 25% Decline In CenterPoint Energy’s stock between 2017 and now?’, has more details on the company’s financials and valuation.

What Could Drive The Stock Higher?

There are a couple of factors that could help CenterPoint stock in the near-term, Firstly, the company is looking to reduce or eliminate its exposure to underperforming segments, such as midstream. CenterPoint’s midstream investments were largely responsible for its dividend cut, as cash flows from the business tumbled following the collapse in energy prices in early 2020. As the company focuses on the more stable utility business, it should bring better earnings visibility, while enabling it to maintain dividends. Secondly, CenterPoint expects earnings growth to be stronger going forward, driven by higher capital expenditures and cost improvements. It upped its annual EPS growth rate target from 5-7% to 6-8% during its investor day event. CenterPoint’s valuation looks attractive, considering the current low-interest-rate environment. The broader utility sector trades at over 18x forward earnings. In comparison, based on consensus 2021 earnings CenterPoint stock trades at just about 15x. Considering this, we think the stock could go higher.

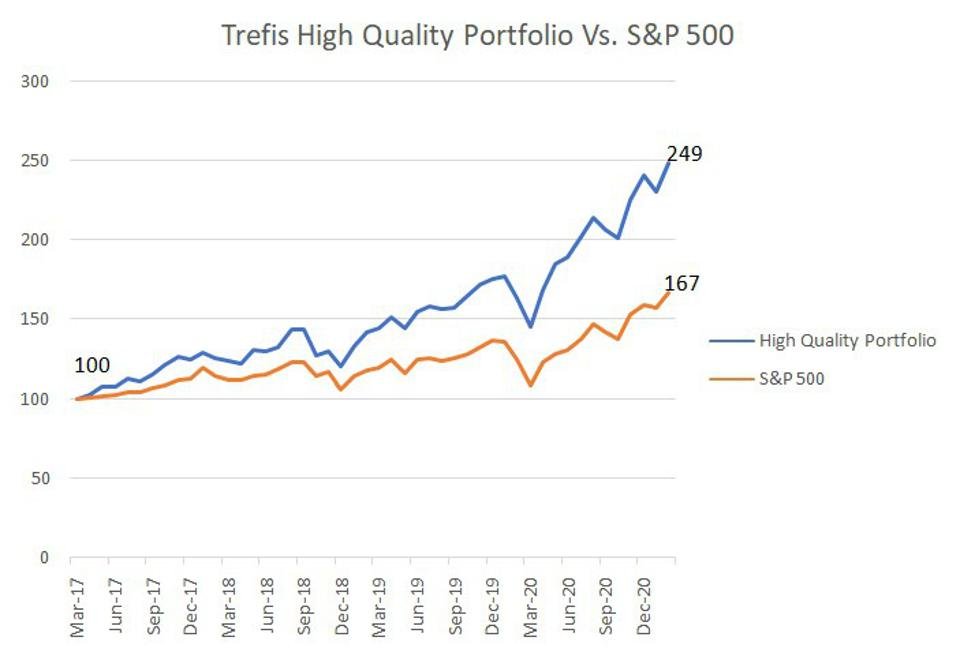

High Quality Portfolio

What if you’re looking for a more balanced portfolio instead? Here’s a high-quality portfolio to beat the market, with over 100% return since 2016, versus 55% for the S&P 500. Comprised of companies with strong revenue growth, healthy profits, lots of cash, and low risk, it has outperformed the broader market year after year, consistently.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams