{kind=link}

The Accenture logo is seen on a building in central Warsaw, Poland on 18, 2019. Accenture, formerly … [+]

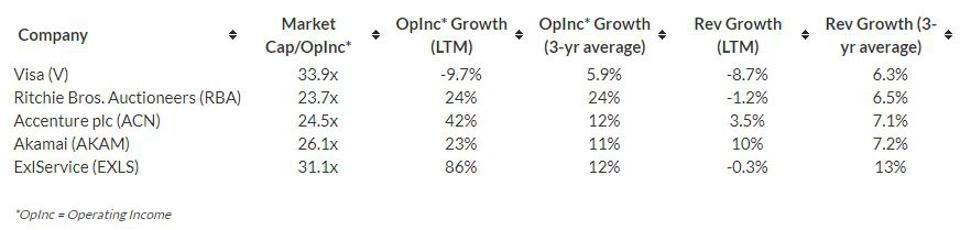

We think that Ritchie Bros. Auctioneers (NYSE: RBA), Accenture plc. (NYSE: ACN), Akamai (NASDAQ: AKAM) and ExlService (NASDAQ: EXLS) stocks are currently better picks compared to Visa (NYSE: V). While all the above stocks are Visa’s peers in the Internet Software & Services Industry, they have given an average return of 25% since the end of 2019, better than the 10% return by Visa and 21% by S&P500 over the same period. Further, each of them has reported faster growth in profits and revenues over the last twelve months and three-year period, as compared to Visa. That said, they still appear to be cheaper than Visa. Despite better profit and revenue growth, these companies have a comparatively lower valuation multiple (market cap-to-operating income ratio) than V (33.9x) – RBA (23.7x), ACN (24.5x), AKAM (26.1x), and EXLS (31.1x). However, there is more to the comparison. Let’s step back to look at the fuller picture of the relative valuations of the above companies by looking at historical revenue and operating income growth as well as respective operating margins. Our dashboard Better Bet Than V Stock has more details on this. Parts of the analysis are summarized below.

Revenue Growth

- Although Visa has the second-highest revenues in the group – next to Accenture, its average annual growth rate of 6.3% over the last three years was the lowest.

- ExlService

EXLS has the highest average annual revenue growth rate of 13% over the same period, followed by Akamai (7.2%), Accenture (7.1%), and Ritchie Bros. (6.5%).

- This implies that Accenture’s revenues have grown at a faster pace than Visa’s, despite being significantly higher than its peer. The remaining three companies are relatively small with annual revenues of less than $5 billion – not comparable with Visa and Accenture in terms of revenues and operating income.

Operating Income

- Visa has a significantly higher operating margin than its peers – 62% in Last-Twelve Months, which was almost 4 times Accenture’s operating margin of 15%. The second best was AKAM with 21%.

- That said, Visa’s average annual growth rate in operating income of 5.9% over the last three years was the lowest among its peers.

- Ritchie Bros. reported the highest annual growth rate of 24% over the same period, followed by EXLS (12%), ACN (12%), and AKAM (11%).

- This implies that Accenture’s operating income has grown at a 2x pace than Visa.

The Net of It All

Visa is a much bigger company as compared to its peers, baring Accenture. While its revenue growth compares unfavorably with its peers over the recent years, its operating margins are much better and stable close to the 60% mark. On the flip side, the payment processing giant is unlikely to see a significant increase or decrease in its revenues over the next 1-2 years. However, its peers may continue to see higher revenue growth than Visa. Further, EXLS, AKAM, and RBA are still in the growth phase. Hence, with better top-line growth along with margin expansion, they will likely post better earnings growth over Visa in the coming years, boding well for their stock. Additionally, we think there is a huge difference between the Price-to-sales (P/S) multiple of Visa (21.1x) and the next in line – Akamai (5.5x), implying that Visa’s stock is quite expensive as compared to RBA, ACN, AKAM, and EXLS.

While Visa Stock may not be attractive, 2020 has created many pricing discontinuities which can offer attractive trading opportunities. For example, you’ll be surprised how counter-intuitive the stock valuation is for Amazon vs Etsy. Another example is Apple vs Microsoft.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams