{kind=link}

Confident business professionals in creative office

Starting now, a combination of five positive drivers can produce an exceptional employment uptrend. And, as unemployment shrinks, optimism will rise, fostering growth.

Here are the five primary drivers for improving employment:

- The coming seasonal uptrend in employment

- The move to Covid-19-free life

- The new Covid-19 government support plan

- The advance preparation by organizations

- The financial system strength

That #1 driver, seasonal uptrend, is a free ride to fuller employment that economists are overlooking. So, more about that below. But first…

How the five drivers can produce growth that exceeds expectations

Importantly, those five drivers can build upon one another:

- The coming seasonal uptrend in employment means a wind-at-the-back for broad-based improvement

- The move to Covid-19-free life means the potential to return to partial or full pre-pandemic activities and employment

- The Covid-19 government support plan provides a foundation for growth

- The advance preparation by organizations means they are primed to build on improving conditions

- The financial system strength means sound organizational strategies can be funded

Now, to understanding the importance of item #1 – seasonal uptrend in employment

Despite the pandemic’s disruption of the economy from March 2020 to now, economists have continued to “seasonally adjust” data. The mistake is that seasonal adjustments only work in normal times – not in recessions and certainly not in pandemics where disruptions are spread unevenly throughout the economy and randomly across the months. The sole reason for altering the real data is to allow comparison between two dissimilar months (say, December and May). That is an inadequate reason for doing so now.

Instead, the evaluation of what’s happening during abnormal times requires using actual (i.e., not seasonally-adjusted – “NSA”) data. Then, introduce any seasonal variations into the analysis by using qualitative judgment.

The January NSA unemployment picture shows the significant potential for employment growth

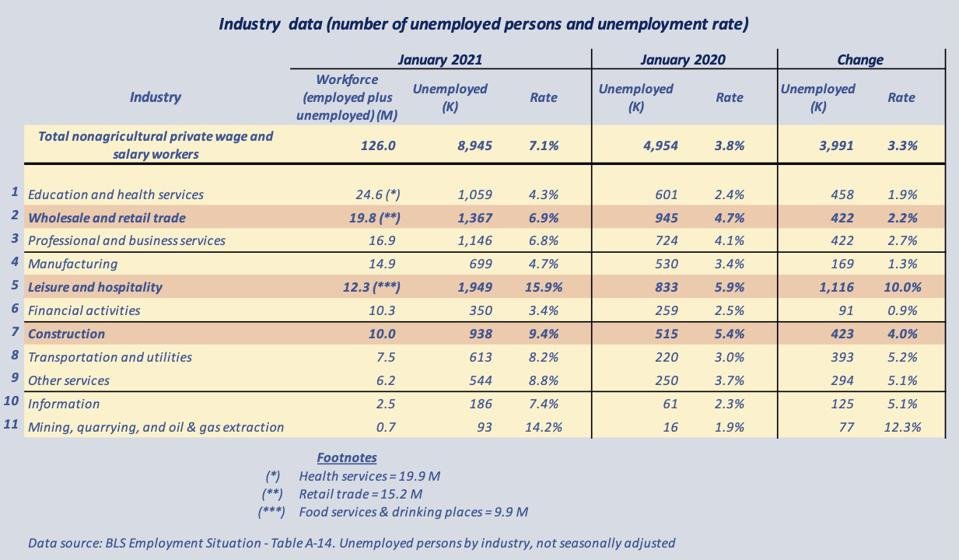

Last Friday’s Bureau of Labor Statistics (BLS) “Employment Situation” report for January provides the data for understanding what could go right in the months ahead. That data, in the table below, show the U.S. unemployment picture in January 2021 compared to the pre-pandemic January 2020 situation. (Comparing two similar months removes the need to consider seasonal variations.)

Note: There are a lot of numbers here, but understanding employment-unemployment dynamics requires digging into the data. The media’s focus on one-number reporting (e.g., the unemployment rate is 6.3%) provides no sense of what might be coming next.

BLS January unemployment data for sectors

From this picture, the “Leisure and Hospitality” category stands out because of its currently high unemployment level (persons looking for a job in the category) and high unemployment rate (the percentage of the workforce).

The three highlighted categories (Wholesale & retail trade, Leisure & hospitality, and Construction) are notable for their higher unemployment amounts. They account for 33% of the nonagricultural, private, wage/salary workforce, but 48% of the unemployed.

The BLS “Leisure and Hospitality” category is a perfect example

This category is composed of three sectors. (NSA data are January employment level and unemployment rate)

- Arts, entertainment & recreation – 1.5 M employees; 19.1% unemployment rate

- Accommodation – 1.4 M employees; 23.1% unemployment rate

- Food services & drinking places – 9.6 M employees; 14.4% unemployment rate

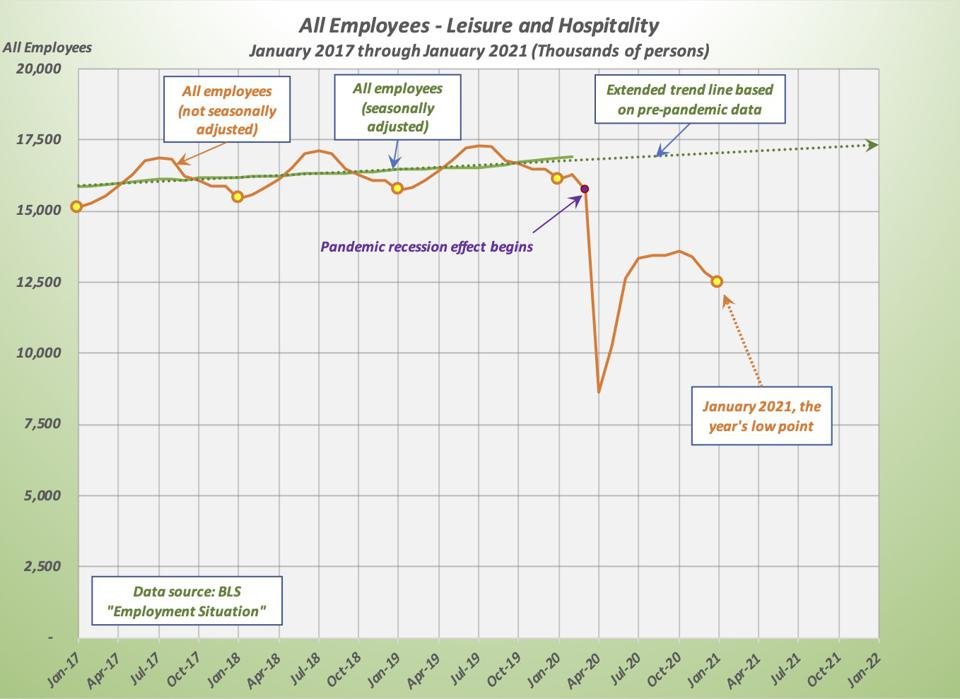

All have strong seasonal shifts in employment with January being the yearly low point. The reason is the combination of the post-holiday and winter slowdowns.

The two graphs below show the seasonal trend for the entire category and how seasonal growth can boost employment.

BLS Leisure & Hospitality monthly employment data

BLS Leisure & Hospitality monthly employment data

The way to evaluate the potential growth is to consider four sources of growth.

First is a moderating of the abnormally low employment due to the pandemic effects. Compared to January 2020’s employment of 16.1 million, January 2021’s 12.5 million is a shortfall of more than 3-1/2 million. As the Covid-19 effects diminish, that employment gap will begin to fill.

Second is the natural seasonal increase up to the summer months. Will it reach the regular 1.5 million level? Even if it doesn’t, there will be significant hiring as places open and business increases.

Third, 2020’s prolonged closures and stay-at-home advice means there should be 2021 growth due to catching up on postponed plans (AKA pent-up demand)

Fourth, even with closures and partial openings, organizations have been altering, remodeling, even expanding with strategies to attract customers. Thus, there is the possible added growth from improved and new offerings of restaurants, bars, hotels, resorts, entertainment, museums, etc.

A final word – Ignore those forecasts of a “new life style”

A popular view is that the benefits of staying, playing, working and eating at home are clear now. Therefore, life-by-internet is here to stay. Well…

Remember that a popular post-Great Recession belief was that the hard times had made savers of us all. No more credit cards. The goal of paying off a 15-year mortgage quickly. Thrift, conservation and a large nest egg was the new life style.

And then we got steady jobs with a decent income. That’s when saving gave way to new “needs” (AKA desires). And back came the mantra, “Don’t wait until tomorrow because tomorrow may not arrive.” So, Disney World, here we come!