{kind=link}

A trader blows bubble gum during the opening bell at the New York Stock Exchange (NYSE) on August 1, … [+]

Like the Dot.Com bubble of the late ‘90s, the typical signs of an approaching bubble bust were on full display in the equity markets last week (week ending January 29th). GameStop

Meanwhile, the GDP did grow 4% (Annual Rate – AR) in Q4 (0.985% Q/Q). Unfortunately, all the growth occurred in October. Economic activity in November and December fell at a -3% AR.

The Economy

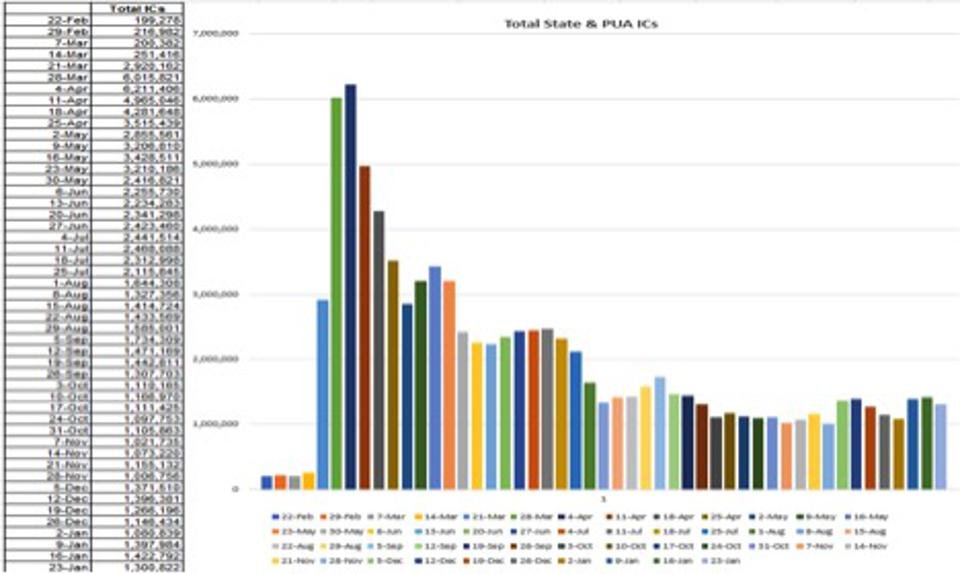

During the week ending January 23rd, state Initial Unemployment Claims (ICs) fell -101K, a hopeful sign.

Total State & PUA ICs

California, alone, was responsible for -64K of that fall. It should be noted that CA showed -59K the prior week and that data was flagged by the Department of Labor as an “estimate.” As a result, the magnitude of the fall in the state programs over the past two weeks is suspect.

Still, the available data (both state and Pandemic Unemployment Assistance programs) show 1.3 million new layoffs in the latest week and from the accompanying chart and table, it is apparent that no real progress on the employment front has been made since September. And that squares with the observation that GDP weakened in November and December. The chart and table show that some employment progress was made in October, and then things flattened in November, and weakened since.

Other data:

· The Conference Board’s Leading Economic Indicators (LEI) show sequential weakening:

- May: +3.10%

- August: +1.62%

- November: +0.74%

- December: +0.27%

· New Home Sales, at 842K (December) was below the consensus estimate of 870K. Prices have been a big issue (median: +8.0% Y/Y; average +4.6% Y/Y), but weakness is appearing, especially in the Northeast. In August, the months’ supply of inventory was a scant 3.5; the latest (December) supply is 4.3 months. The starts/sales ratio has risen to 1.59 meaning that for every two homes sold, there are more than 3 new starts. Unless demand picks up, this could spell future weakness.

· In the GDP report, DPI (Disposable Personal Income) fell -9.5% (AR) in Q4 after declining -16.9% (AR) in Q3. The fact that Consumption grew +2.5% (AR) in Q4 in the GDP report is entirely due to a fall in the savings rate.

Pent-Up Demand

In my last few blogs I discussed my view that the pent-up demand narrative will be a dud. To reiterate, the narrative is that, once the vaccine is well distributed (assumed to be end of Q2), pent-up demand will launch the economy.

· The math says herd immunity, via the vaccine, won’t occur until sometime in mid-2022, not Q3/2021.

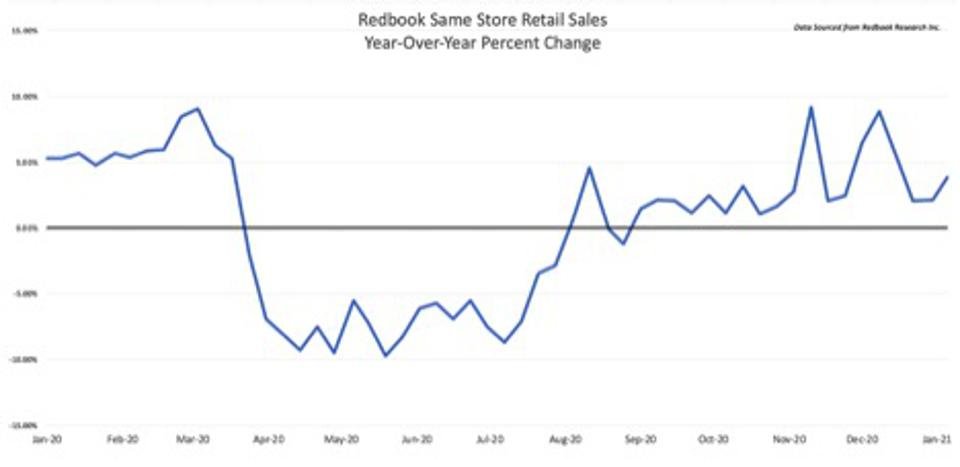

· Retail sales have fallen three months in a row through January. The higher than “normal” expenditures for the “stay at home” economy (appliances, furniture, home-improvement) through the fall have now turned negative as the consumer has become satiated. In the chart, compare the typical growth in retail spending in January and February 2020 to the low level of sales growth in Q4. There were a couple of weeks of sales spikes in the holiday period, but minimal growth otherwise.

· Income, too was an issue, as “stimulus” cash gifts did not return until late December. In the face of the fall in goods demand, when the economy reopens, how will the “pent-up” demand for travel, restaurants, and events (6% of consumptions; 4% of GDP) launch the economy to new heights?

Redbook Same Store Retail Sales

· 18 million people, out of a labor force of 165 million (11%), are unemployed. Do you think these folks are going to rush out to restaurants, buy airline tickets and go on vacation, or visit a casino when they have back-rent due and no job? Even when Uncle Same gives them additional “stimulus” money, most of it will be saved. Recent NY Fed data indicate that 71% of such “stimulus” will go into debt repayment (credit card balances are down 10% Y/Y) or other forms of saving (including playing in the stock market).

· Recent data also shows that average wages are rising while the median measure is falling. This has occurred because job losses are concentrated in the ranks of the lower wage earners, thus raising the average. Of course, when this occurs, income inequality widens. Also realize that it is the lower wage earners who consume their entire paychecks, while upper wage earners save some. This fact plays poorly in the pent-up demand narrative.

· There are a few bright spots. One is manufacturing (<15% of GDP). Core cap-ex orders (non-defense capital goods ex aircraft) were up 0.6% in December after rising 1.0% in November. Expenditures on tech equipment rose a very significant 10.5% Y/Y in December.

Inflation

The narrative that inflation is imminent remains just that, a narrative. After an initial spike from 0.93% to 1.15% from January 4th to January 11th, the 10-Year U.S. Treasury Bond fell back to 1.04% and closed at 1.07% on Friday, January 29th. It doesn’t appear that the bond market is buying into the inflation narrative.

The Fed isn’t threatening to raise rates, in fact, quite the opposite. They are committed to the 0% bound and to a continuation of liquidity injections (asset purchases) until inflation rises to at least 3%. They just reiterated that position in the presser after their recent January meetings. At this time, the NY Fed’s inflation forecast index stands at 1.49%; a year ago it was 2.31%. The Cleveland Fed’s 10-year inflation expectation index is 1.38%. A year ago it was 1.73%.

We have seen some spikes in the prices of commodities, but these are mainly supply constraints imposed by the virus. The three main components of the Consumer Price Index (CPI), accounting for 44% of the index and 55% of the “core” index, are medical care, education, and rents. For the first time in the history of the data series, going back to the 1950s, medical care prices have fallen three months in a row. The costs of education, via tuition, which had been rising briskly year in and year out, are now stagnant to falling due to declining enrollments (students choosing to sit out a year rather than pay handsomely for on-line classes). And rents, alone accounting for 30% of CPI, are contracting because of the abandonment of large cities and delinquencies. Inflation occurs when rents, wages and credit demands are strong. None of that exists in today’s economy.

Economic Conclusions

Employment remains the biggest issue. Even the complete lifting of all business restrictions won’t resolve this anytime soon. Too many small businesses have closed permanently and large employers are likely to rehire slowly. For many reasons, the pent-up demand narrative remains that, only a narrative. It is also foolish to believe that one day we will wake up and everyone will act as if things are back to pre-virus “normal.” Equity markets have priced such a return to “normal” as occurring in Q3/2021. Again, nonsense. And while the future seeds of inflation are currently being sown, it isn’t imminent or close to imminent, and it won’t be until the demand and employment gaps are closed. That is several years off.

Bubble, Bubble

As indicated at the top of this blog, the recent market action driving up the prices of Wall Street’s most shorted stocks is of the type typically seen at the peak of bubbles. GameStop (GME) for example, had a recent market cap of $28 billion, a joke compared to the underlying value of its actual business and the cash flow (negative in this case) generated. Other market data also are indicative of a speculative blow-off. In the week ended January 30, 2021, U.S. equity volume was 23x the average weekly level in 2020, and options volume was 10x higher.

GME is the poster-child for these speculative excesses. On August 2, 2020, the stock closed at $4.87/share. As of December 24th, it had risen to $20.15, and then to $43.03 on January 21st. Over the last six trading days (ending January 29th) it rose to $347.51 (January 27th), fell to $193.60 (January 28th), and then rebounded to $325 (January 29th). This gives the company a $22.7 billion market cap. Sounds incredible! The problem is, there is no underlying earnings/cash flow to support such a valuation. And the company trends are negative. In 2016, revenues were $9.4 billion and pre-tax profits were +$647 million. Sales, for the 12 months ended in October 2020, fell to $5.2 billion and 2019 profits were -$471 million. Even if the company survives, its valuation is nuts. The only way today’s investor in this stock can make money is via the “greater fool” theory, i.e., someone more foolish will pay a higher price.

Most intelligent investors put money on a company if they think that sales/earning are or will be strong, not because some social media website told them to. But that is what we have. In this case, is a man, known as “Roaring Kitty,” whose real name is Keith Gill, via websites Reddit and WallStreetBets (WSB) convinced thousands of social media followers to purchase GME. (He made a $53,000 investment in GME in 2019.) He did that because GME was one of the most highly shorted listed companies. By acting as a cabal, the WSB crowd pushed up the price of the stock to such an extent that the large hedge funds, which had shorted it based on its fundamentals, took huge losses. Melvin Capital, a highly respected hedge fund, got crushed to the tune of 30% of its value during the week. Of course, when such large funds are forced to cover, that adds to the upward price pressures. This stock has risen to what appears to be unsustainable heights. (Caution – while the current price appears unsustainable, it can still go higher – look at Bitcoin.) By the way, Roaring Kitty’s stock, if he still has it all, is reportedly worth north of $40 million- if he can find a greater fool to purchase it at that price. I doubt he can.

Meanwhile, there was some political brouhaha over the fact that some of the trading sights, including Robinhood (the 1st choice of the “stay at home” momentum investors), stopped margin trading in that shorted-stock group. By SEC rules, account holders may borrow up to 50% of the value of the marginable equities in their account (not all equities are marginable), and that allows leverage. When stocks get so volatile that their prices fluctuate wildly – by 50% in a short period of time, the lender is at risk of capital loss. Under such conditions, sites, like Robinhood, have potential problems with their clearing firms regarding capital requirements. So, some sites, including Robinhood, shut down trading in GME and other such stocks and took them off the list of marginable equities. This brought on the ire of both the social media crowd, and even some Washington pols who thought it unfair that the “little guy” should be restricted just when he/she has the apparent advantage over the Wall Street hedge fund titans. They are going to have Congressional hearings on this. I doubt much will change. By Friday, the stocks were trading (and rising) again, but they couldn’t be purchased on margin.

This saga isn’t over – stay tuned. Such behavior is almost always a sign that the bubble is ready to burst. To be sure, this behavior isn’t the same as we saw in the dot-com episode of 1999 – 2000. Back then investors drove up the prices of Amazon, Cisco, and even Yahoo in the belief that these companies had real potential. Looking back, they were right about Amazon. Cisco still trades around its price back then, and Yahoo, while still alive, is private. Today’s behavior is similar only by the fact that it is extreme. Otherwise, it is truly bizarre. Perhaps it is emulating today’s cancel culture – in this sense, to cancel (or at least be the opposite of) Wall Street. Still, we always see foolish behavior right at bubble peaks. So, no – this time is not different – trust me!