{kind=link}

WASHINGTON, July 31, 2019 (Xinhua) — U.S. Federal Reserve Chairman Jerome Powell reacts during a … [+]

There was quite a spike in interest rates the last week of February with the 10-Year T-Note spiking from a 1.36% level as of the close on Wednesday to as high as 1.60% intraday with a close of 1.55% on Thursday. Friday’s close was 1.45%. But, a lot of damage was done.

It is naïve to think this spike was caused by the inflation narrative, i.e., that rates would spike because of inflation expectations. The latest inflation expectations from official Fed forecasts show that those expectations are coming down, not going up. In addition, at this stage of the cycle, equities would welcome higher inflation. But, no! Equity prices reacted poorly to the interest rate spike.

Immediate Cause

The immediate cause of the rate spike was the worst 7-year Treasury auction on record (i.e., the lowest bid to cover ratio). Notable was the lack of any Japanese participation, likely Chinese too. And with the upcoming massive “stimulus” package that passed the House of Representatives early Saturday morning (February 27), markets are seeing massive new debt that is likely to cause indigestion unless the Fed steps in with new rounds of QE. In addition, on Sunday (February 28), several significant Fed programs are due to end. Do you think Powell (and Yellen) will let those expire? We don’t, and we sense that the Fed will make some pronouncements before the end of the first week of March. If they don’t, they risk significant damage to the nascent recovery.

Labor Markets

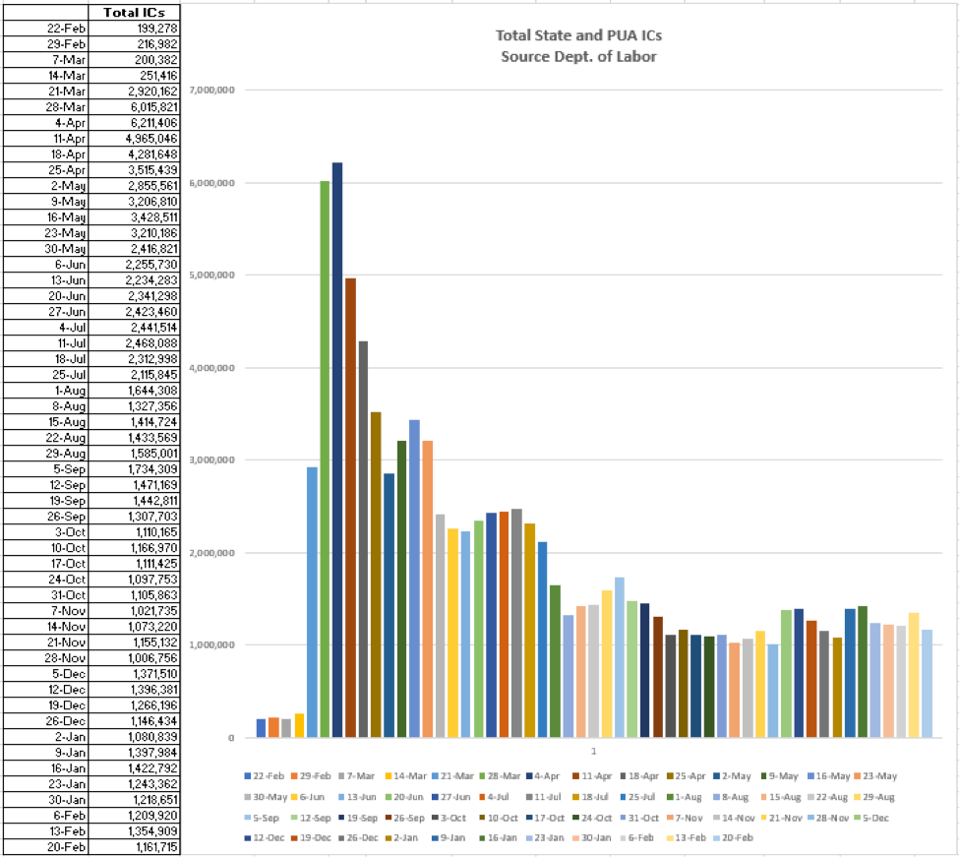

At first blush, the weekly Department of Labor Initial Unemployment Claims (ICs) for the week of February 22 looked like good news, as there was a large down-spike in state ICs. The aggregated state numbers (not seasonally adjusted) fell to 710K from 842K (revised down from 862K) the prior week. Part of the apparent improvement in ICs may have been due to weather in Texas and/or to audits in Ohio ferreting out fraudulent claims. California also had a very large down-spike (re-openings?). Ohio, California and Texas accounted for 79% of the -132K improvement.

There was also some improvement (-61K) in the Pandemic Unemployment Assistance (PUA) programs which saw ICs drop to 451K (week of February 22) from 513K. Together, the state and PUA programs had 1.16 million net new claims (a proxy for weekly layoffs). This takes us back to levels not seen since October, and is a positive sign that the easing of restrictions on businesses is having a positive impact.

Total State and PUA ICs

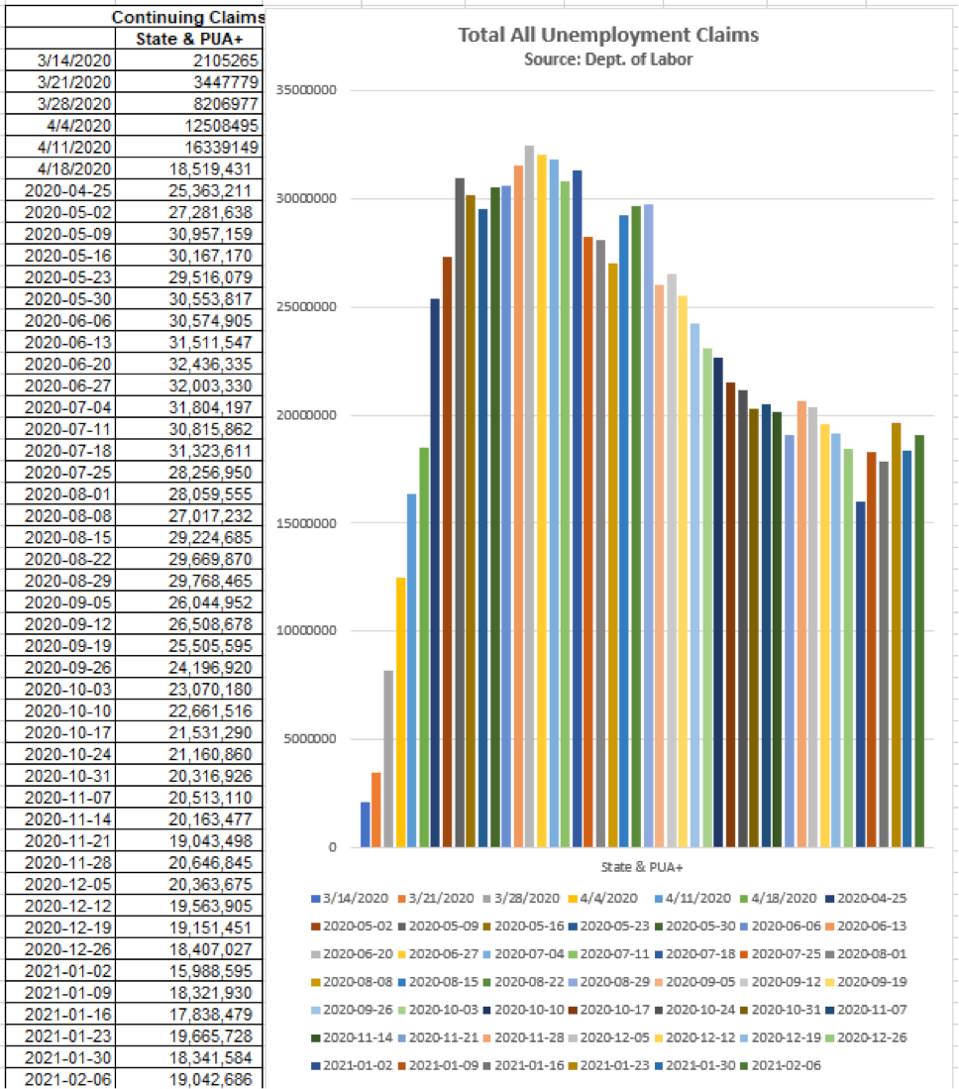

The next chart and table show Continuing Unemployment Claims (CCs) (those claiming benefits for more than one week). The latest data is for the week of February 6. In this series, there was a rise back to more than 19 million. With the rollout of the vaccines and more widespread business re-openings, the IC numbers should continue to improve, and, hopefully, we will also see a turnaround in the CC data. The real question here is how much damage to the economy has been done and how many of those 19 million lost jobs are permanent.

Total All Unemployment Claims

Inflation is a Process

As seen from the above, the labor markets, while showing some initial signs of improvement, continue to be quite weak. Undoubtedly, some of the upcoming “stimulus” will find its way into GDP. But without such “helicopter money,” organic demand would not be there. And that means that, until the labor markets heal, a sustained inflation is unlikely.

Yes, there can be spikes in the CPI. Today, commodity shortages (some of which are caused by transportation delays) can push up some prices. So can weather (i.e., energy price spikes in Texas). And, we are entering a three-month period where there will be Y/Y comparisons to some very depressed prices at the pandemic’s start. Remember the few days of negative oil prices? So, CPI may be elevated through May. But, inflation is a process consisting of demand consistently exceeding supply. With 19 million unemployed (and an additional seven million labor force drop outs who would like a job), it is difficult to envision an imminent demand surge.

Pent-Up vs. Pent-Down

We saw significant increases in spending on goods in 2020, as consumers, stuck with little ability to receive services, purchased stuff (home-improvement goods (increased sales at Home Depot

In addition, due to the federal government’s “stimulus” programs, Personal Disposable Income grew more than 5% in 2020, a year of the worst GDP decline since 1946 and the worst unemployment levels in the country’s history. There was “stimulus” in April/May and again in December, and the upcoming package is even more generous. No doubt, GDP will grow (Atlanta Fed says Q1 will grow at 9.5%; most other economic forecasts are in the 5%-6% range). But that is due to borrowed money (like spending on one’s credit card). Because unemployment is likely to be significant for the foreseeable future, without continued “stimulus,” the inflation process won’t take hold.

Surveys

Survey after survey indicates deteriorating expectations and buying intentions. The latest University of Michigan Consumer Sentiment and Conference Board Consumer Confidence reports show the following:

- Buying intentions for autos have declined to the lowest level since October 2008;

- Household intentions to purchase a major appliance are at the lowest level since September 2011;

- Buying plans for homes are down to their lowest level since the April/May 2020 pandemic induced recession, and before that, once again to levels not seen since October 2008.

Cost of Debt

In addition, Pending Home Sales, a reliable leading indicator of housing activity, has flattened. That’s not a wonder. In December, the S&P Core Logic Home Price Index rose +1.30% M/M (+16.3% annualized). It is up +10.4% Y/Y. And the spike in the 10-Year T-Note discussed above, will also have an impact, as mortgage rates are closely tied to that yield. Doing some quick math, a 1-percentage point rise from 3% to 4% in the 30-year fixed rate on a $300,000 mortgage increases the monthly payment from $1,265 to $1,432. That’s money not available for consumption.

Taking that logic a bit further, the explosion of debt recently, and especially since the beginning of the pandemic, has raised the level of U.S. debt (all levels from governments to businesses to households) to $80 trillion. A 1-percentage point rise in rates will eventually cost the economy $800 billion in additional interest. That’s 4% of GDP, hardly affordable.

Bank Lending

As indicated in past blogs, bank lending has fallen since the initial April/May line of credit drawdowns when businesses, worried that banks would cancel their lines of credit, drew on those lines to put cash on their balance sheets. Since then, loans and leases have fallen and banks have been huge net buyers of Treasury debt. So far in 2021, the latest bank data show that Loan and Lease levels, Mortgages, and Consumer Loan balances have all been falling. The inflation process has never occurred in an environment where credit is contracting.

The Fed’s Own Inflation Calculus

- The Philly Fed forecasts 2.2% 10-year inflation;

- The NY Fed’s leading inflation gauge is 1.5% (was 2.2% a year ago);

- The Cleveland Fed’s 5-year inflation expectation measure is 1.42% (1.62% a year ago);

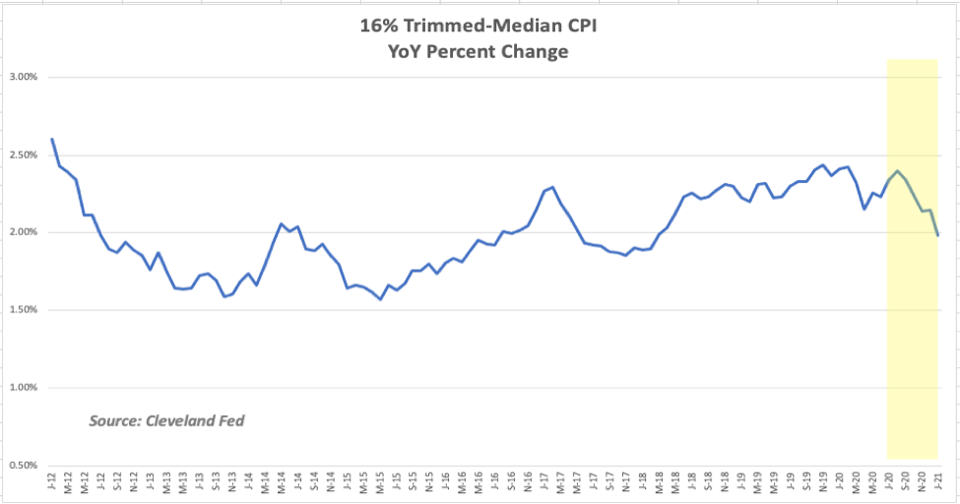

- The chart shows the Cleveland Fed’s 16% Trimmed-Median CPI. This is the median of the data after the top and bottom 8% of observations are eliminated. The Y/Y percent change is near 2% as shown in the chart, down from nearly 2.5% a year earlier. The January M/M annualized change was +0.7%

16% Trimmed-Median CPI; YoY Percentage Change

Conclusions

- The interest rate spike in the Treasury yield curve is due to the excessive amount of current and prospective debt rather than to worries about inflation;

- Labor markets eased a bit toward the end of February; perhaps re-openings. It is hard to tell the degree to which state audits and weather played a role. Hopefully, improvements will continue;

- However, it is unlikely that, in the foreseeable future, the unemployment level will be reduced to the point of inducing inflation. And, while there are likely upcoming spikes in the CPI, the inflation “process” remains dormant;

- Surveys show a significant pullback of household intentions to purchase big ticket items, and bank lending, a prerequisite for inflation, is falling;

- All the regional Fed inflation models indicate continued deflationary pressures. Of course! Between 19 million and 26 million people remain unemployed!

- The spike in rates will damage the nascent recovery! Where’s the Fed?