{kind=link}

POLAND – 2020/10/20: In this photo illustration a American Express logo seen displayed on a … [+]

[Updated 02/08/2021] American Express Valuation Update

After more than an 80% gain since the March 23 lows of the last year, we believe that American Express stock (NYSE: AXP) has limited upside. Trefis estimates American Express’s valuation to be around $130 per share – approximately 5% above the current market price. American Express is a global financial services company, which offers charge and credit card products along with travel-related services to consumers and businesses across the globe. While the company surpassed consensus estimates in its recently released fourth-quarter results, its revenues dropped 18% y-o-y to $9.35 billion. It could be attributed to an 18% y-o-y drop in non-interest revenues due to lower consumer spending and a drop in discount rate, followed by a 17% decline in net interest income.

American Express is the third-largest player in card transaction volume in the U.S. and derives the majority of its revenues from discount fees – around 57% in 2020. The fee is charged as a % of card transactions that take place with partner merchants. Hence, the company is very sensitive to changes in consumer spending patterns. Due to the Covid-19 crisis, the consumer spending levels dipped, hurting American Express’ top-line. Further, the company has co-branding card arrangements with several hotel chains and airlines. The hotel occupancy rates and the global travel industry were directly impacted by the Coronavirus outbreak. Overall, the above factors negatively impacted American Express’ revenue prospects in 2020, restricting the figure to $36.1 billion – down by 17%. That said, the consumer spending levels have seen some recovery over the recent quarters. Further, the mass availability of the Covid-19 vaccine and improvement in economic conditions over the coming months will likely increase card transaction volumes. It is likely to benefit the company’s top-line, enabling American Express’s revenues to touch $40 billion in FY 2021.

The operating expenses as a % of revenues rose from 72.4% in 2019 to 75% in 2020. Further, the company increased its provisions for credit losses to $4.7 billion for the full year 2020, as compared to $3.6 billion in the year-ago period. As a result, the adjusted net income figure took a hit of 54% on a year-on-year basis, reducing the EPS to $3.77. However, as the economy moves toward normalcy, provisions for credit losses are likely to see some decrease. Additionally, American Express is likely to start its share repurchase program in the first quarter of 2021. This will likely enable the EPS figure to touch $6.84 in FY2021. Overall, the EPS of $6.84 coupled with the P/E multiple of just below 19x will lead to a valuation of around $130.

[Updated 08/06/2020] American Express Stock Gained 38% Over Recent Months, Is It Still Attractive?

American Express stock (NYSE: AXP) lost more than 44% – dropping from $123 at the end of 2019 to around $69 in late March – then spiked 38% to around $95 now. This implies it’s still 23% lower than at the start of the year.

This can be attributed to 2 factors: The Covid-19 outbreak and economic slowdown meant that market expectations for 2020, and the near-term consumer demand, dropped. This could negatively affect the company’s top and bottom line due to a significant decline in card spending on travel, hotels, and other discretionary items coupled with increased exposure to potential loan defaults. The multi-billion-dollar Fed stimulus provided a floor, and the stock recovery owes much to that.

But this isn’t the end of the story for American Express’ stock

Trefis estimates American Express’ valuation to be around $104 per share – about 10% above the current market price – based on an upcoming trigger explained below and one risk factor.

The trigger is an improved trajectory for American Express’ revenues over the second half of the year. We expect the company to report $36.7 billion in revenues for 2020 – around 16% lower than the figure for 2019. Our forecast stems from our belief that the economy is likely to open up in Q3. The easing of lockdown restrictions in most of the world is likely to help consumer demand, resulting in higher spending. The company has co-branding card arrangements with several hotel chains and airlines, e.g., Delta Air Lines

Thereafter, American Express’ revenues are expected to improve to $40.7 billion in FY2021, mainly due to higher discretionary consumer spending on travel, hotels, and other items. Further, the net income margin is likely to improve as compared to the previous year due to a decline in provisions for credit losses, leading to an EPS of $6.66 for FY2021.

Finally, how much should the market pay per dollar of American Express’ earnings? Well, to earn close to $6.66 per year from a bank, you’d have to deposit about $725 in a savings account today, so around 110x the desired earnings. At American Express’ current share price of roughly $95, we are talking about a P/E multiple of around 14x. And we think a figure closer to 16x will be appropriate.

That said, consumer finance is a risky business right now. Growth looks less promising, and near-term prospects are less than rosy. What’s behind that?

American Express is the third-largest player in card transaction volumes in the U.S. Further, it has a sizable portfolio of consumer and commercial card loans – around $83 billion in FY2019. The economic downturn could negatively affect the loan repayment capability of its consumers, exposing the company to significant loan defaults. As a result of this exposure, American Express has increased its provisions for loan losses to around $4.2 billion by Q2 2020– roughly 2.5x of the year-ago period, leading to a huge spike in total expenses for the year. If the economic condition worsens, this figure could further increase in the subsequent months.

The same trend is visible across American Express’ peer – Capital One. Its revenues are likely to suffer in FY2020 due to a drop in consumer spending. Further, its margins are likely to drop due to build-up in provisions for credit losses in anticipation of bad loans. This would explain why Capital One’s stock currently has a price of $65 but looks slated for an EPS of around $7.20 in FY2021.

Trefis

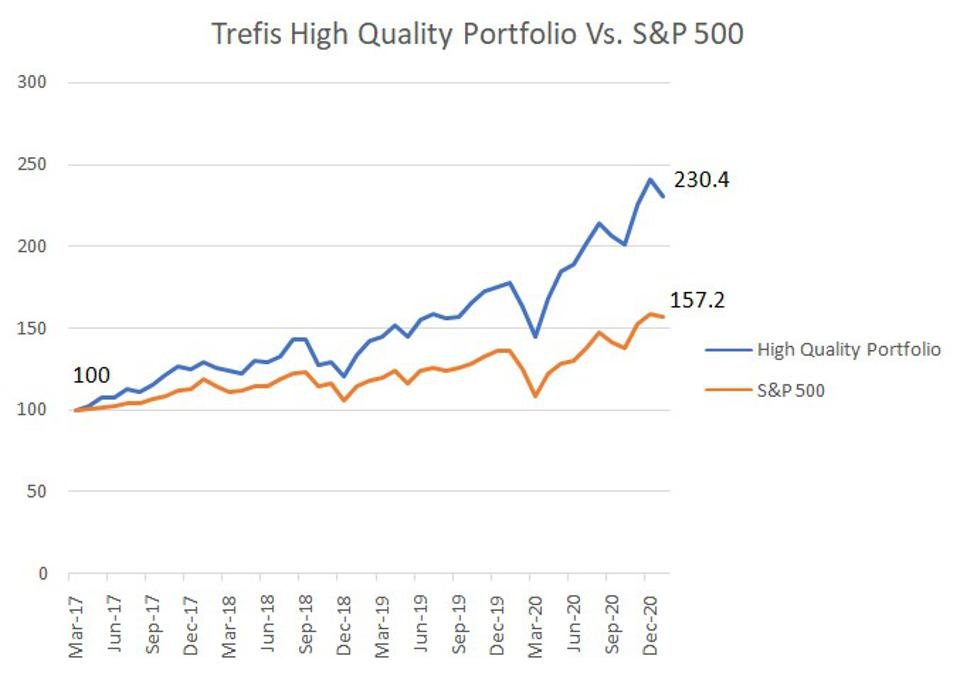

What if you’re looking for a more balanced portfolio instead? Here’s a high quality portfolio to beat the market, with over 100% return since 2016, versus 55% for the S&P 500. Comprised of companies with strong revenue growth, healthy profits, lots of cash, and low risk, it has outperformed the broader market year after year, consistently.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams